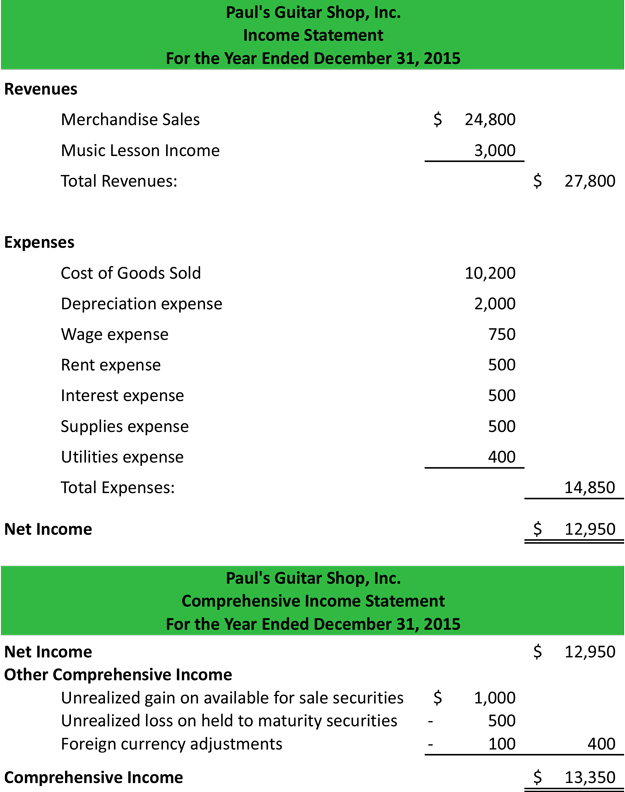

Comprehensive income is generally defined as a change in a companys net assets which can be accredited to the events which are not under the owners control. Besides using the basic formula of determining. Net income or net earnings from the companys income statement. Total comprehensive income is therefore equal to net income other comprehensive income 50 million 25 million 75 million. Gross Profit Margin Revenue COGS. Breaking Down Comprehensive Income. Statement of Comprehensive Income refers to the statement which contains the details of the revenue income expenses or loss of the company that is not realized when a company prepares the financial statements of the accounting period and the same is presented after net income on the companys income statement. The net income is transferred down to the CI statement and adjusted for the non-owner transactions we listed above to compute the total CI for the period. A single statement or. Comprehensive Income Net Income Other Comprehensive Income OCI.

Profit or loss is determined once all the expenses of the company. This number is then transferred to the balance sheet as accumulated other comprehensive income. Under IFRS other comprehensive income also includes certain changes in the value of long-lived assets that are measured using the revaluation model. In its most basic form. Entities may present all items together in. The accounting treatment of comprehensive income is. Other comprehensive income which consists of positive andor negative amounts for foreign currency translation and hedges and a few other items. Whereas other comprehensive income consists of all unrealized gains and losses on assets that are not reflected in the income statement. The statement of comprehensive income covers the same period of time as the income statement and consists of two major sections. It provides an overview of revenues and expenses including taxes and interest.

The statement of comprehensive income covers the same period of time as the income statement and consists of two major sections. Comprehensive Income in Financial Statements. Which of the following is least likely an item that is treated as other comprehensive income. Income Statement Formula. The income statement is one of the major financial statement for a business which shows its expenses Revenue profit and loss over a period of time. Profit or loss is determined once all the expenses of the company. Comprehensive income for a corporation is the combination of the following amounts which occurred during a specified period of time such as a year quarter month etc. Calculating comprehensive income can present a corporation with valuable info about the all round financial stability of the business. Net income or net earnings from the companys income statement. Comprehensive Income Formula Use the following comprehensive income formula.

Calculating comprehensive income can present a corporation with valuable info about the all round financial stability of the business. In its most basic form. Comprehensive Income Gross Profit Margin Operating Expenses - Other Income items - Discontinued Operations add if savings subtract if loss. Statement of Comprehensive Income refers to the statement which contains the details of the revenue income expenses or loss of the company that is not realized when a company prepares the financial statements of the accounting period and the same is presented after net income on the companys income statement. Other comprehensive income which consists of positive andor negative amounts for foreign currency translation and hedges and a few other items. Entities may present all items together in. Breaking Down Comprehensive Income. Profit or loss is determined once all the expenses of the company. Realized holding gains and losses on available-for-sale securities. The net income is transferred down to the CI statement and adjusted for the non-owner transactions we listed above to compute the total CI for the period.

It provides an overview of revenues and expenses including taxes and interest. Realized holding gains and losses on available-for-sale securities. A single statement or. The Basics of Comprehensive Income OCI and AOCI The differences between comprehensive income OCI and AOCI are subtle yet critically important. Profit or loss is determined once all the expenses of the company. Which of the following is least likely an item that is treated as other comprehensive income. Statement of Comprehensive Income refers to the statement which contains the details of the revenue income expenses or loss of the company that is not realized when a company prepares the financial statements of the accounting period and the same is presented after net income on the companys income statement. In addition using the basic formula of determining comprehensive income provides an easy to understand snapshot of how the company has fared since the last analysis. The statement of comprehensive income covers the same period of time as the income statement and consists of two major sections. The accounting treatment of comprehensive income is.