The asset disposal results in a direct effect on the companys financial statements. Gain or loss is computed by subtracting the assets net book value from the cash proceeds. The latter is illustrated in this publication. Under the indirect method the cash flow statement adds the loss on sale or disposal of fixed assets in the net income to calculate the cash flow from operating activities. In that initial reconciliation the profit before tax is adjusted for expenses that have been charged against profit that are not cash out flows. When an organization writes off a fixed asset a bookkeeper debits the loss on asset write off account -- which accountants often classify in the unusual losses category -- and credits the corresponding tangible asset account. Loss on Disposal of Assets. The actual cash inflows and outflows associated first with the assets purchase followed by the assets disposal are accounted for on the cash flow statement as investing cash flows. Loss gain on disposal of fixed assets cash flow statement. Cash received is shown as an asset in balance sheet.

The loss account affects the companys income statement the financial data summary that chronicles corporate profits and losses. The cash impact is the cash proceeds received from the transaction which is not the same amount as the gain or loss that is reported on the income statement. What we want to see for the statement of cash flows is the actual cash received from the sale. Also it is a non-cash expense. The amount of the profit on the disposal of an asset will be shown in the statement of profit or loss as an increase in the years results ie it will have been credited in the statement of profit and loss and thus the profit for the year will be increased. A gain or loss on the disposal of an asset will affect the profit of an entity in the period of disposal. Disposal of a Fixed Asset with Zero Gain or Loss. The assets book value has little relationship with its fair market value. Also this is an item which will be listed under cash flows from investing activities. An entity can present its cash flow statement using the direct or indirect method.

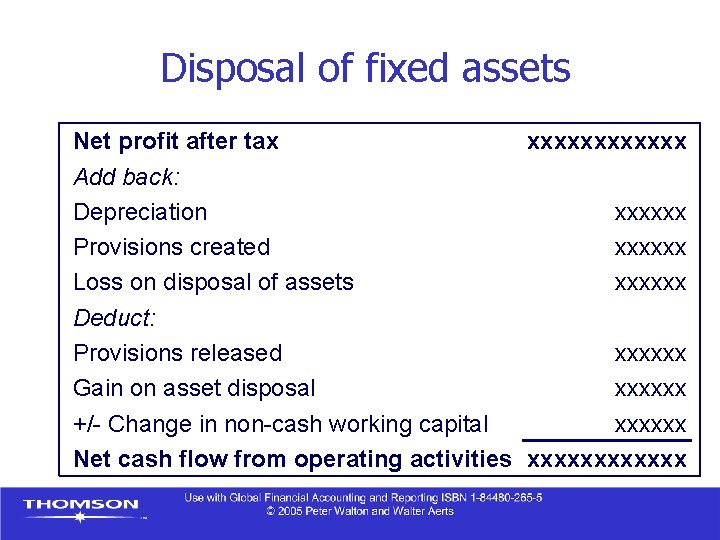

- Impairment loss on financial assets available-for-sale 575 - Net gain on disposal of financial assets available-for-sale 200. Also if a company disposes of assets by selling with gain or loss the gain and loss should be reported on the income statement. Gain or loss is computed by subtracting the assets net book value from the cash proceeds. Also it is a non-cash expense. The latter is illustrated in this publication. Under the indirect method the cash flow statement adds the loss on sale or disposal of fixed assets in the net income to calculate the cash flow from operating activities. A gain or loss on the disposal of an asset will affect the profit of an entity in the period of disposal. Cash Flow Statement Cash flow from operating activities indirect method Net income increase in current assets - decrease in current assets increase in current liabilities decrease in current liabilities - gain on disposal of long term assets - loss on disposal of long term assets depreciation amortization. What is the amount of the gain or loss on. Net book value is the assets original cost less any related accumulated depreciation.

A loss in disposal of plant asset is shown in income statement as an expense Subtracted from our profit. Gain or loss is computed by subtracting the assets net book value from the cash proceeds. A gain or loss on the disposal of an asset will affect the profit of an entity in the period of disposal. For example depreciation and losses on disposal of non-current assets have to be added back and non-cash income. When an organization writes off a fixed asset a bookkeeper debits the loss on asset write off account -- which accountants often classify in the unusual losses category -- and credits the corresponding tangible asset account. Loss on disposal is shown as an expense. Under the indirect method the cash flow statement adds the loss on sale or disposal of fixed assets in the net income to calculate the cash flow from operating activities. Disposal of a Fixed Asset with Zero Gain or Loss. Loss gain on disposal of fixed assets cash flow statement. In that initial reconciliation the profit before tax is adjusted for expenses that have been charged against profit that are not cash out flows.

An entity can present its cash flow statement using the direct or indirect method. Net book value is the assets original cost less any related accumulated depreciation. Depreciation and loss on disposal of assets are both expense items found on the income statement while EBITDA earnings before interest taxes depreciation and amortization is a measure of income that is often reported as a discrete item on the income statement although it is not required to be under generally accepted accounting principles or GAAP. In all scenarios this affects the balance sheet by removing a capital asset. For example investment income and profits on disposal of non-current assets are deducted. Cash received is shown as an asset in balance sheet. The actual cash inflows and outflows associated first with the assets purchase followed by the assets disposal are accounted for on the cash flow statement as investing cash flows. The assets book value has little relationship with its fair market value. Reduces profit but does not impact cash flow it is a non-cash expense. The asset disposal results in a direct effect on the companys financial statements.