Ace Private Company Goodwill Impairment Governmental Financial Statements

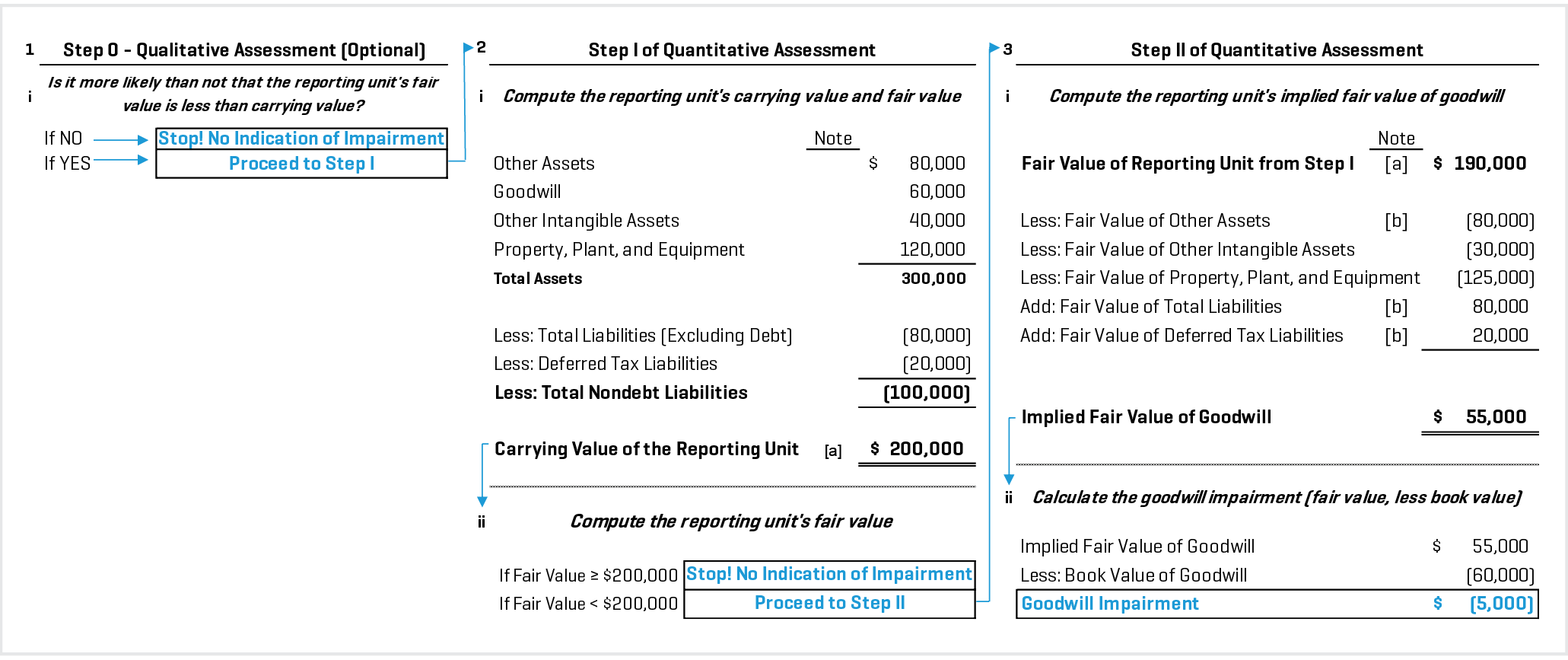

Eliminating Step Ii Streamlining Goodwill Impairment Testing Stout

Privately held company data for making informed investment decisions with conviction. Now private companies will amortize goodwill over a maximum of 10 years. Only the parents share of the goodwill impairment loss will actually be recorded ie 60 x 50 30. A shorter life can be. Examples of triggering events include the loss of a key customer unanticipated competition or negative cash flows from operations. Per accounting standards goodwill is recorded as an intangible asset and evaluated periodically for any possible impairment in value. Instead goodwill will be. However impairment testing was complicated and many users of the financials of private companies told the PCC that they simply disregarded goodwill and its impairment. The impairment loss will be applied to write down the goodwill so that the intangible asset of goodwill that will appear on the group statement of financial position will be 270 300 30. Under private company treatment rather than carrying goodwill on the books at its original value and testing it for impairment annually private companies may elect to amortize goodwill on a straight-line basis over 10 years or less if the company demonstrates that.

Privately held company data for making informed investment decisions with conviction.

A shorter life can be. Examples of triggering events include the loss of a key customer unanticipated competition or negative cash flows from operations. Private companies that elect this alternative are not required to test goodwill for impairment each year but theyre still required to test goodwill for impairment when a triggering event happens. Under private company treatment rather than carrying goodwill on the books at its original value and testing it for impairment annually private companies may elect to amortize goodwill on a straight-line basis over 10 years or less if the company demonstrates that. Private companies can however elect to amortize the goodwill that they have acquired in business combinations on a straight-line basis over 10 years or less if the entity demonstrates that another useful life is more appropriate and can elect to use a. A shorter life can be.

Specifically the ASU gives a private company or NFP the option to perform the goodwill impairment triggering event evaluation required by ASC 350-202 as well as any resulting goodwill impairment test as of the end of the entitys interim or annual reporting period as applicable. Upon electing the accounting alternative private companies are required to make an accounting policy election to test goodwill for impairment at either the entity level or the reporting-unit level. Goodwill impairment triggering event alternative which allows eligible entities to perform the goodwill impairment triggering event analysis and any resulting impairment test required by ASC 350-20 IntangiblesGoodwill and Other Goodwill as of the end of each reporting period whether an interim or annual reporting period instead of performing that analysis throughout the reporting period and any resulting impairment. Goodwill is acquired and recorded on the books when an entity purchases another entity for more than the fair market value of its assets. Now private companies will amortize goodwill over a maximum of 10 years. Only the parents share of the goodwill impairment loss will actually be recorded ie 60 x 50 30. Ad Combine private company data with our investment research for comprehensive insights. For public companies the cost is well worth the benefit of better looking financials remember no amortization higher profits. A shorter life can be. If elected ASC 350 requires certain disclosures which differ from those discussed in FSP 89.

Under private company treatment rather than carrying goodwill on the books at its original value and testing it for impairment annually private companies may elect to amortize goodwill on a straight-line basis over 10 years or less if the company demonstrates that. ASU 2021-03 provides an accounting alternative for private companies and not-for-profit entities to assess goodwill impairment triggering events only at reporting dates interim or annual. Private companies can however elect to amortize the goodwill that they have acquired in business combinations on a straight-line basis over 10 years or less if the entity demonstrates that another useful life is more appropriate and can elect to use a. Ad Combine private company data with our investment research for comprehensive insights. Under the alternative private companies no longer will be required to perform annual goodwill impairment testing. Goodwill impairment triggering event alternative which allows eligible entities to perform the goodwill impairment triggering event analysis and any resulting impairment test required by ASC 350-20 IntangiblesGoodwill and Other Goodwill as of the end of each reporting period whether an interim or annual reporting period instead of performing that analysis throughout the reporting period and any resulting impairment. The FASBs new goodwill impairment testing guidanceASU 2017-04 required for public SEC filers for periods beginning after December 15 2019while intended as a simplification could result in less precise goodwill impairments for reporting entities. Instead goodwill will be. Instead it will be tested for impairment only when a triggering event occurs indicating the fair value of the entity or reporting unit may be below its carrying amount. Private companies and NFPs can elect the alternative regardless of whether they have elected to apply the accounting alternative for the subsequent measurement of goodwill ie the accounting alternative for amortizing goodwill.

Examples of triggering events include the loss of a key customer unanticipated competition or negative cash flows from operations. Private companies can however elect to amortize the goodwill that they have acquired in business combinations on a straight-line basis over 10 years or less if the entity demonstrates that another useful life is more appropriate and can elect to use a. Instead it will be tested for impairment only when a triggering event occurs indicating the fair value of the entity or reporting unit may be below its carrying amount. FASB finalizes private company alternative for timing of goodwill triggering event assessment. However impairment testing was complicated and many users of the financials of private companies told the PCC that they simply disregarded goodwill and its impairment. What is Goodwill Impairment. Ad Combine private company data with our investment research for comprehensive insights. Private companies and NFPs can elect the alternative regardless of whether they have elected to apply the accounting alternative for the subsequent measurement of goodwill ie the accounting alternative for amortizing goodwill. Upon the occurrence of a triggering event a simpler one-step impairment test will be performed. Ad Combine private company data with our investment research for comprehensive insights.

Many private companies evaluate the entire reporting period for goodwill impairment as part of their annual reporting process. Performing this evaluation at year-end makes it difficult to determine whether a goodwill impairment triggering event occurred during the reporting period and creates challenges in recognizing and measuring any resulting goodwill impairment charge as of the. FASB finalizes private company alternative for timing of goodwill triggering event assessment. The impairment loss will be applied to write down the goodwill so that the intangible asset of goodwill that will appear on the group statement of financial position will be 270 300 30. Now private companies will amortize goodwill over a maximum of 10 years. Goodwill is acquired and recorded on the books when an entity purchases another entity for more than the fair market value of its assets. Goodwill impairment triggering event alternative which allows eligible entities to perform the goodwill impairment triggering event analysis and any resulting impairment test required by ASC 350-20 IntangiblesGoodwill and Other Goodwill as of the end of each reporting period whether an interim or annual reporting period instead of performing that analysis throughout the reporting period and any resulting impairment. However for smaller private companies the incremental impairment test cost is significant. Upon the occurrence of a triggering event a simpler one-step impairment test will be performed. Private companies and NFPs can elect the alternative regardless of whether they have elected to apply the accounting alternative for the subsequent measurement of goodwill ie the accounting alternative for amortizing goodwill.

Goodwill is acquired and recorded on the books when an entity purchases another entity for more than the fair market value of its assets. Under the alternative private companies no longer will be required to perform annual goodwill impairment testing. If elected ASC 350 requires certain disclosures which differ from those discussed in FSP 89. Per accounting standards goodwill is recorded as an intangible asset and evaluated periodically for any possible impairment in value. Private companies and NFPs can evaluate goodwill for impairment only as of their reporting dates 1 April 2021. Upon electing the accounting alternative private companies are required to make an accounting policy election to test goodwill for impairment at either the entity level or the reporting-unit level. However for smaller private companies the incremental impairment test cost is significant. Privately held company data for making informed investment decisions with conviction. Instead it will be tested for impairment only when a triggering event occurs indicating the fair value of the entity or reporting unit may be below its carrying amount. For public companies the cost is well worth the benefit of better looking financials remember no amortization higher profits.